2026 Factsheets

April 2026 Factsheet

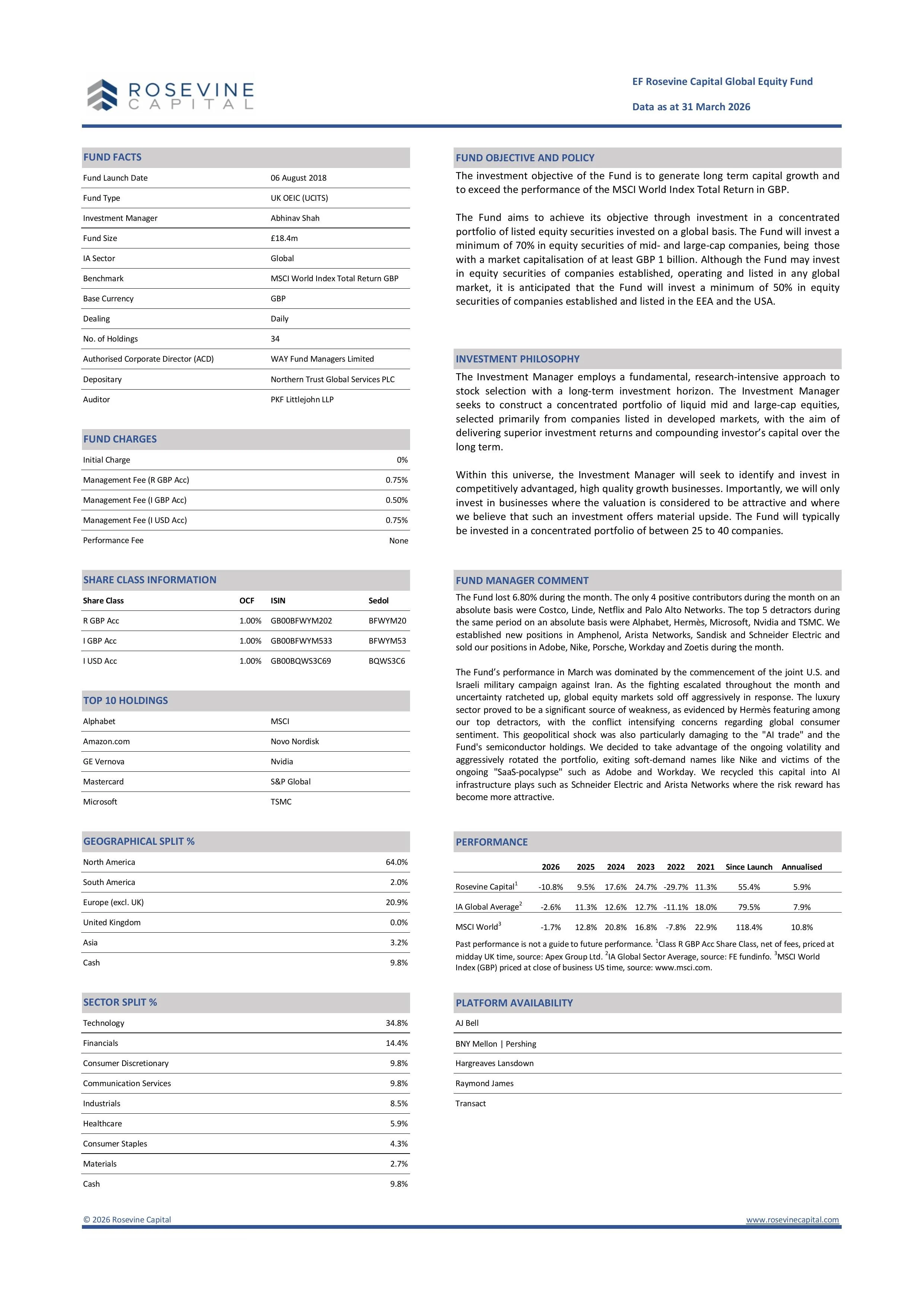

March 2026 Factsheet

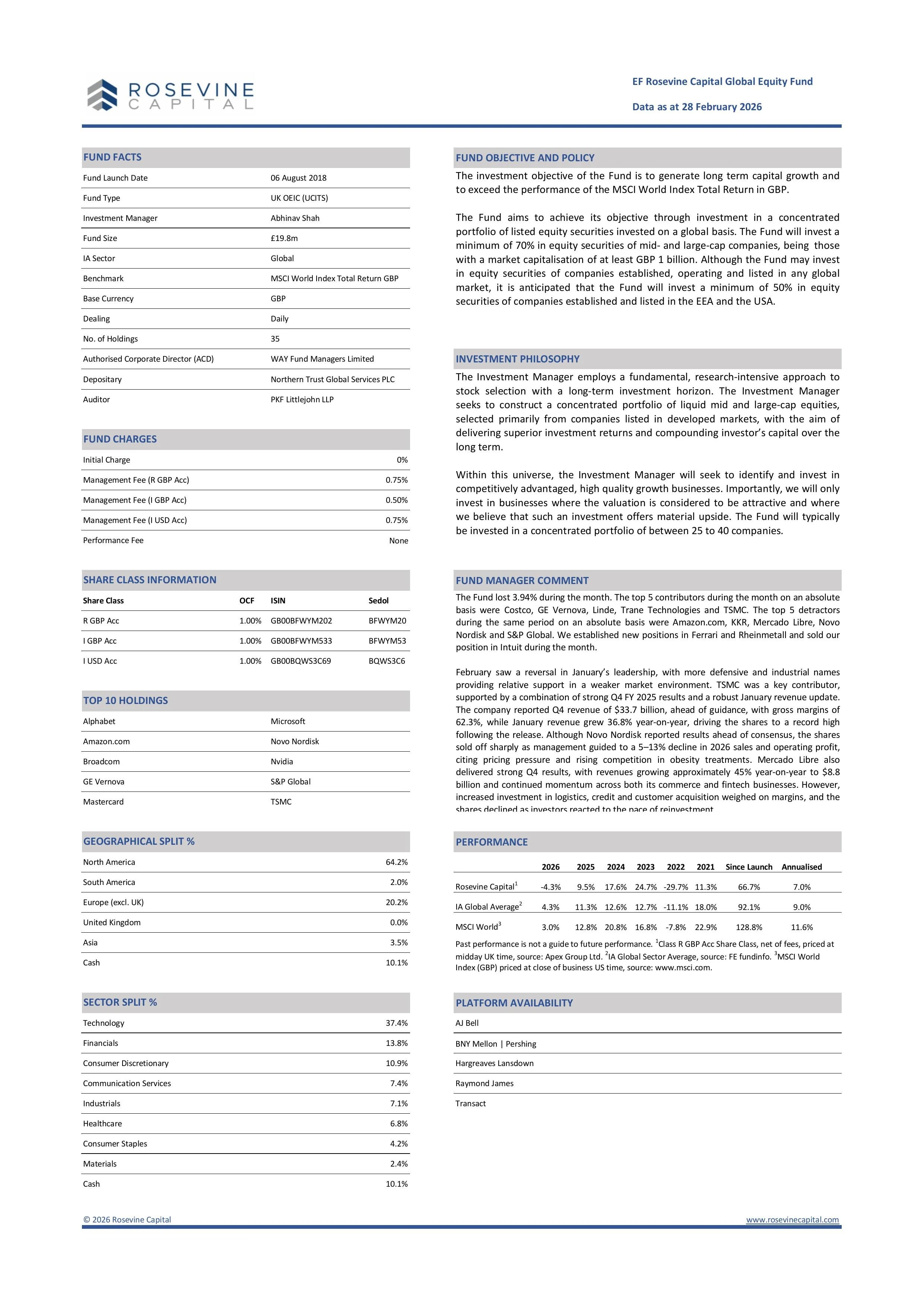

February 2026 Factsheet

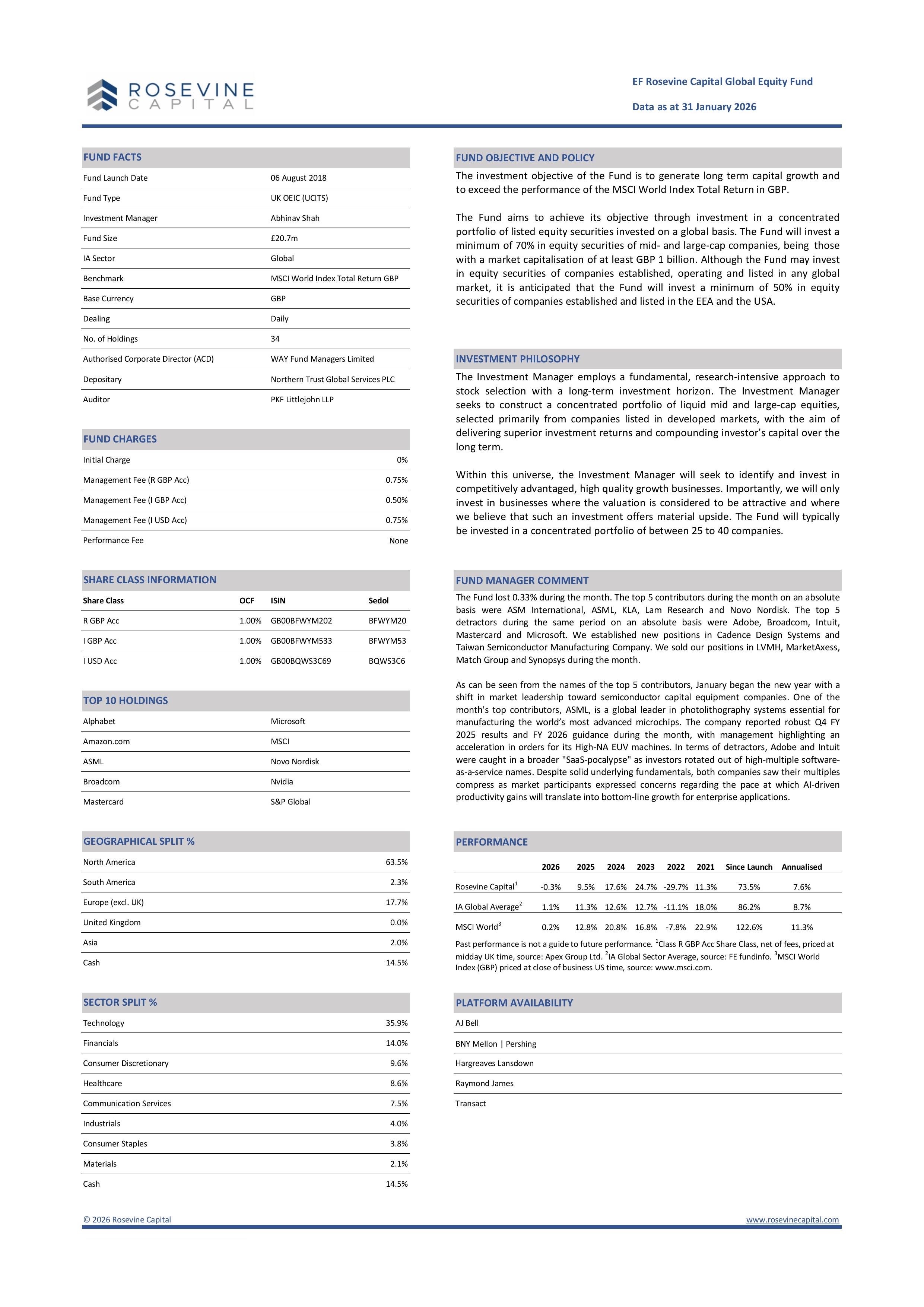

January 2026 Factsheet

2025 Factsheets

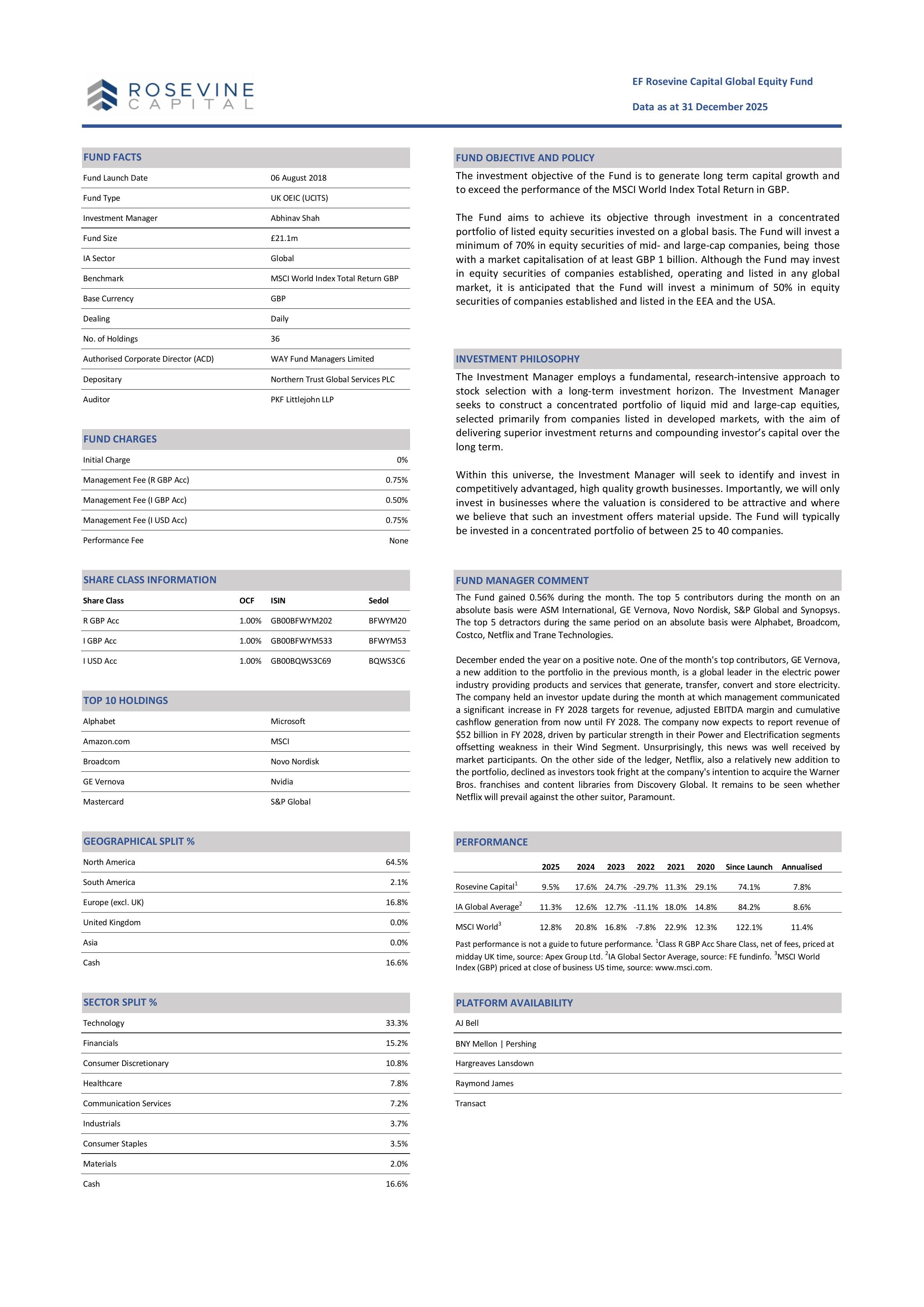

December 2025 Factsheet

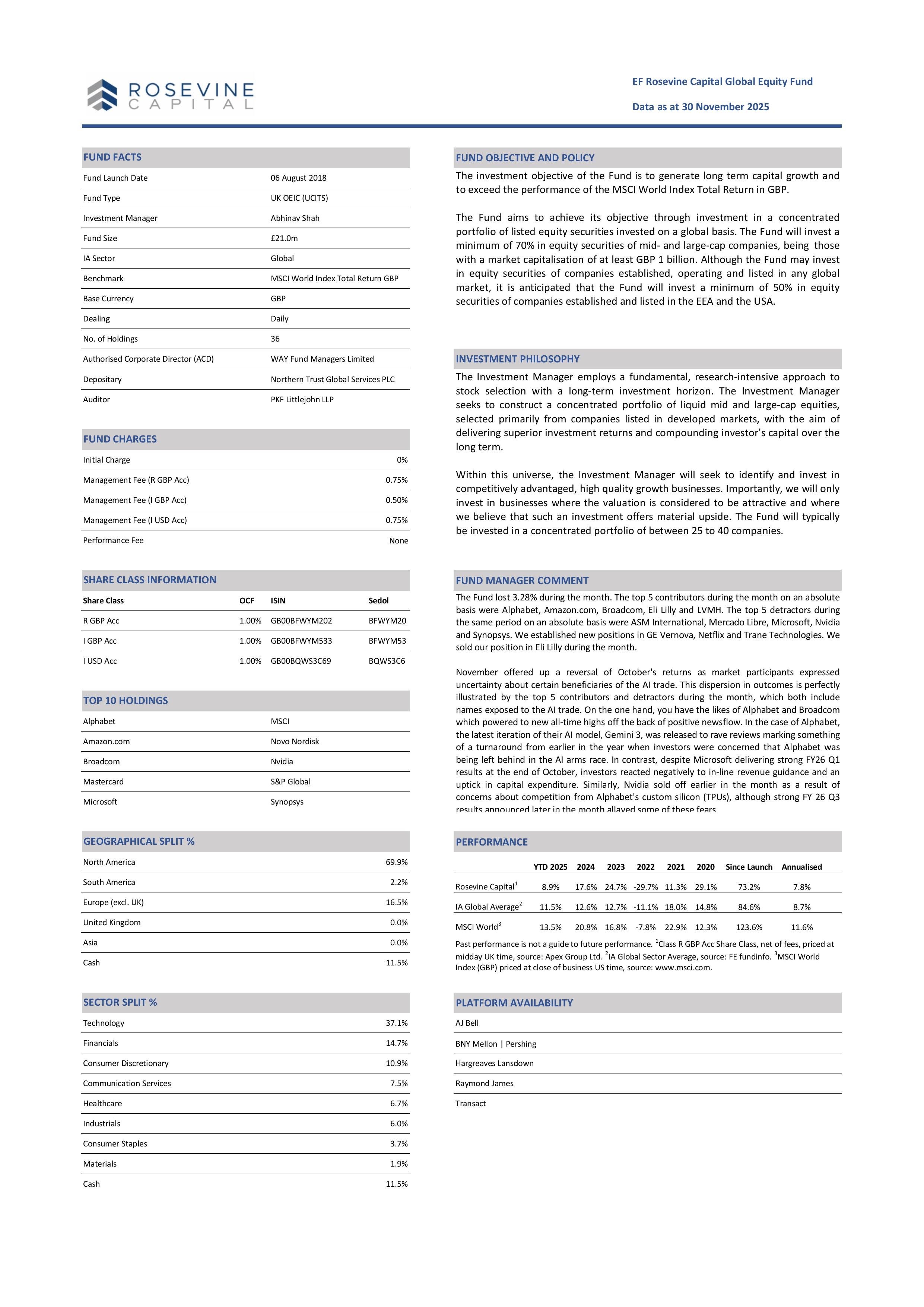

November 2025 Factsheet

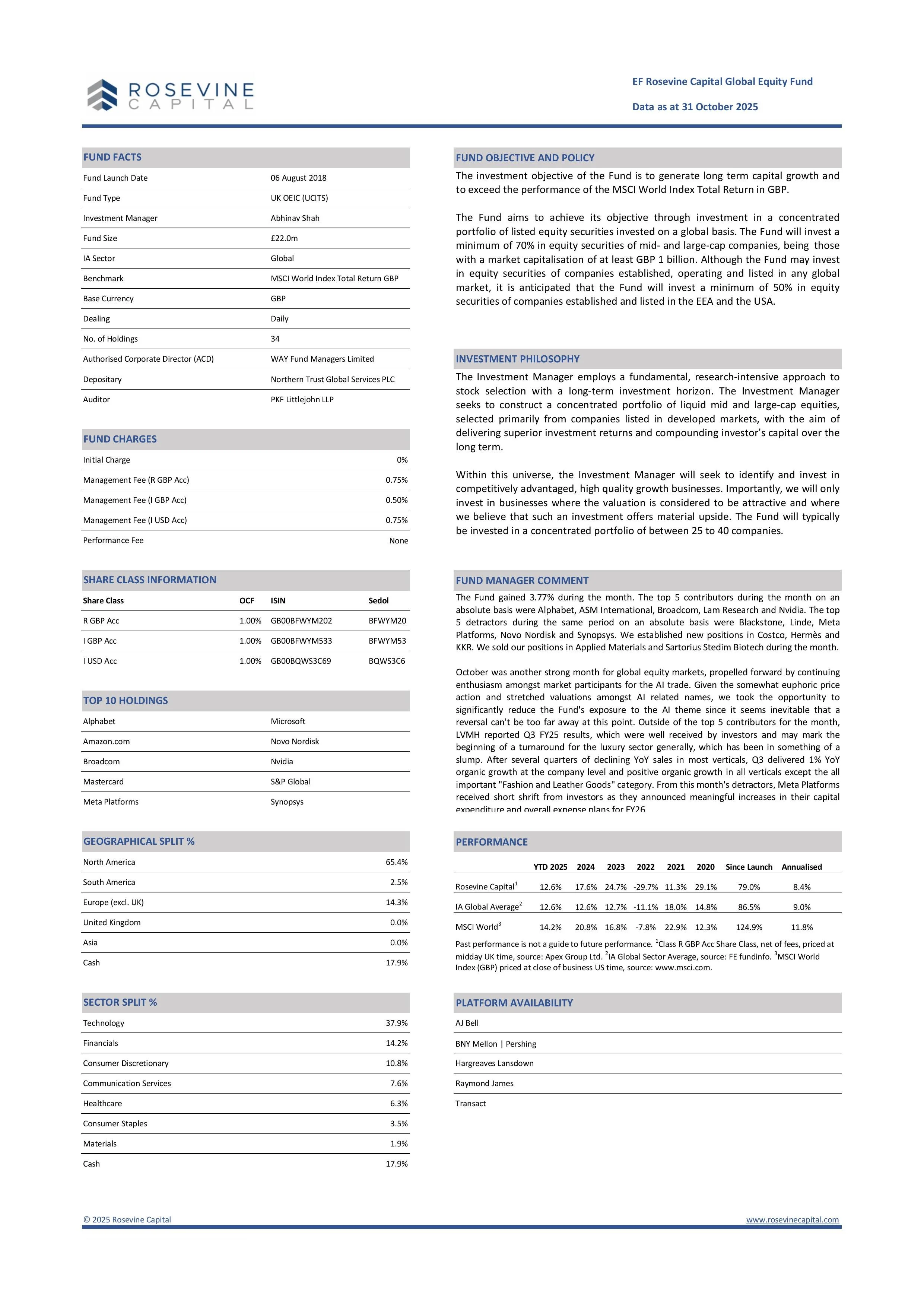

October 2025 Factsheet

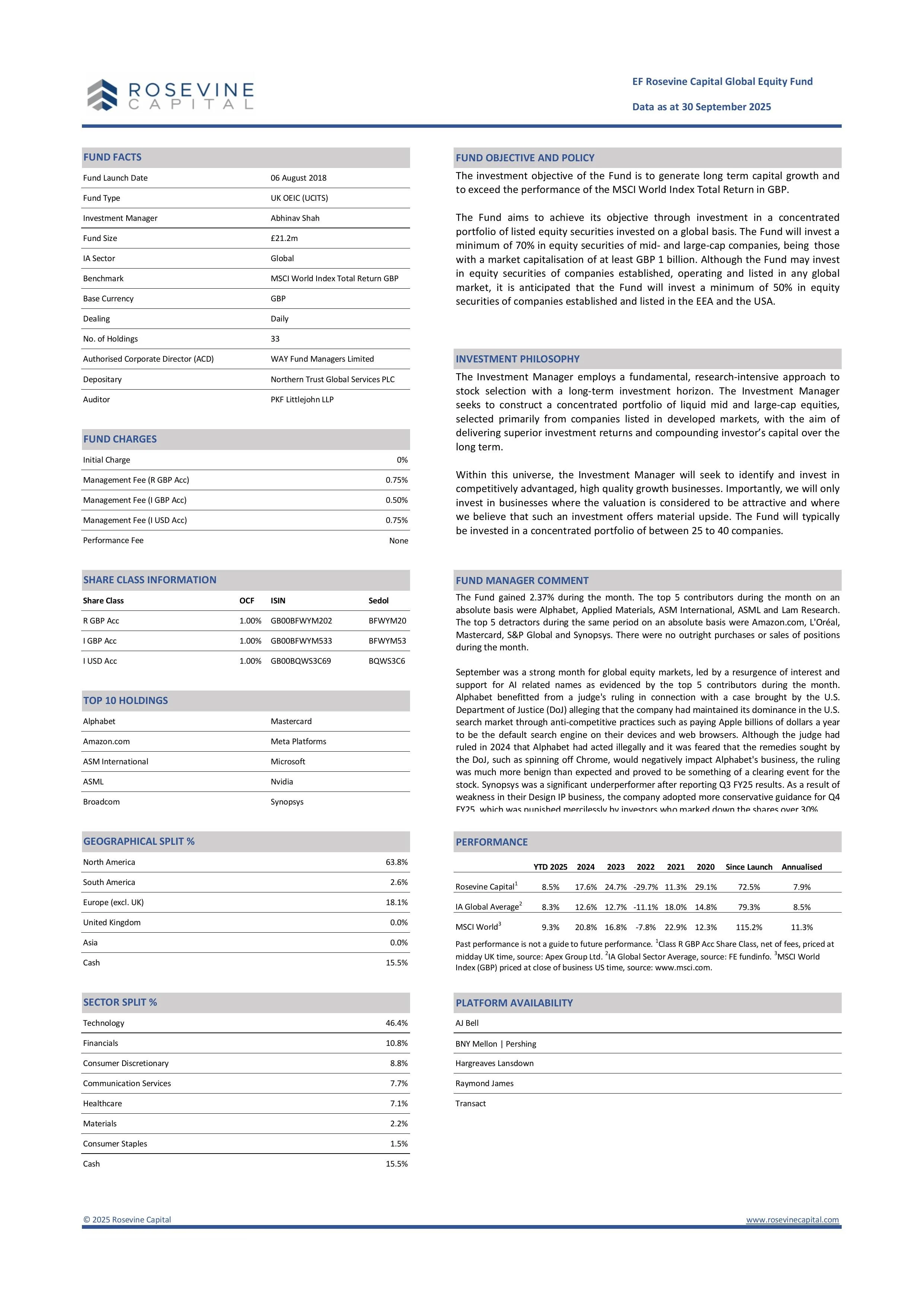

September 2025 Factsheet

August 2025 Factsheet

July 2025 Factsheet

June 2025 Factsheet

May 2025 Factsheet

April 2025 Factsheet

March 2025 Factsheet

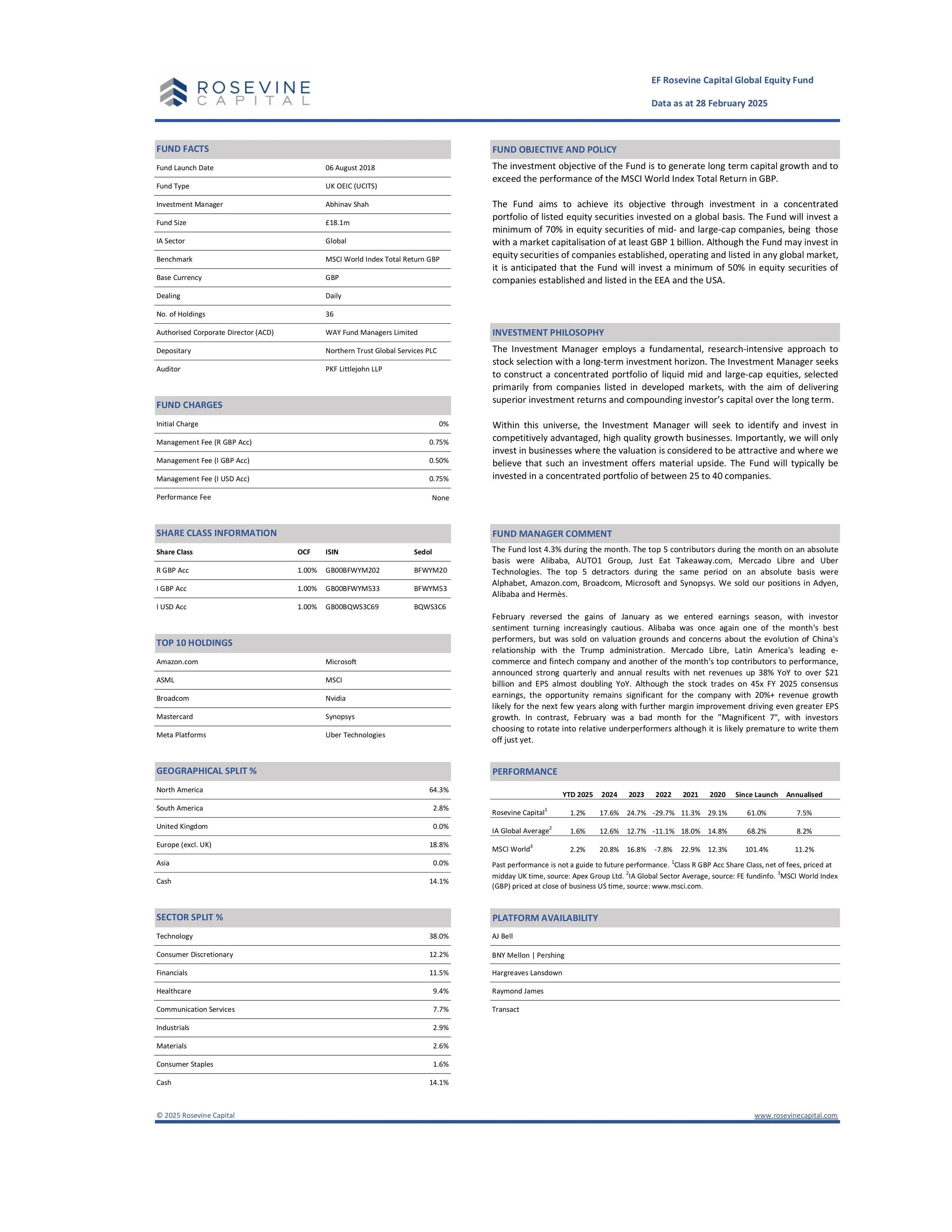

February 2025 Factsheet

January 2025 Factsheet

2024 Factsheets

December 2024 Factsheet

November 2024 Factsheet

October 2024 Factsheet

September 2024 Factsheet

August 2024 Factsheet

July 2024 Factsheet

June 2024 Factsheet

May 2024 Factsheet

April 2024 Factsheet

March 2024 Factsheet

February 2024 Factsheet

January 2024 Factsheet

2023 Factsheets

December 2023 Factsheet

November 2023 Factsheet

October 2023 Factsheet

September 2023 Factsheet

August 2023 Factsheet

July 2023 Factsheet

June 2023 Factsheet

May 2023 Factsheet

April 2023 Factsheet

March 2023 Factsheet

February 2023 Factsheet

January 2023 Factsheet

2022 Factsheets

December 2022 Factsheet

November 2022 Factsheet

October 2022 Factsheet

September 2022 Factsheet

August 2022 Factsheet

July 2022 Factsheet

June 2022 Factsheet

May 2022 Factsheet

April 2022 Factsheet

March 2022 Factsheet

February 2022 Factsheet

January 2022 Factsheet

2021 Factsheets

December 2021 Factsheet

November 2021 Factsheet

October 2021 Factsheet

September 2021 Factsheet

August 2021 Factsheet

July 2021 Factsheet

June 2021 Factsheet

May 2021 Factsheet

April 2021 Factsheet

March 2021 Factsheet

February 2021 Factsheet

January 2021 Factsheet

2020 Factsheets

December 2020

November 2020

October 2020 Factsheet

September 2020 Factsheet

August 2020 Factsheet

July 2020 Factsheet

June 2020 Factsheet

May 2020 Factsheet

April 2020 Factsheet

March 2020 Factsheet

February 2020 Factsheet

January 2020 Factsheet

2019 Factsheets

December 2019 Factsheet

November 2019 Factsheet

October 2019 Factsheet

September 2019 Factsheet

August 2019 Factsheet

July 2019 Factsheet

June 2019 Factsheet

May 2019 Factsheet

April 2019 Factsheet

March 2019 Factsheet

February 2019 Factsheet

January 2019 Factsheet

2018 Factsheets

December 2018 Factsheet

November 2018 Factsheet

October 2018 Factsheet

September 2018 Factsheet

| undefined | |

|---|---|

| Fund Launch Date | 6th August 2018 |

| Fund Type | UK OEIC (UCITS) |

| IA Sector | Global |

| Base Currency | Sterling |

| Benchmark | MSCI World Index Total Return GBP |

| Share Classes | GBP R Acc: GB00BFWYM202 |

| GBP I Acc: GB00BFWYM533 | |

| USD I Acc: GB00BQWS3C69 | |

| Management Fee | GBP R Acc - 0.75% per annum |

| GBP I Acc - 0.50% per annum | |

| USD I Acc - 0.75% per annum | |

| Performance Fee | No |

| Dealing | Daily |

| Authorised Corporate Director (ACD) | WAY Fund Managers Limited |

| Depositary | Northern Trust Global Services PLC |

| Auditors | PKF Littlejohn LLP |

Before investing, please make sure you have read the UCITS Key Investor Information Document for the EF Rosevine Capital Global Equity Fund – Class I (GBP Acc), Class I (USD Acc) and Class R (GBP Acc). If you are unsure as to the suitability of an investment for your circumstances, please seek independent financial advice. Please note that investments can go down in value as well as up.

You can invest in the fund directly through WAY Fund Managers Limited by calling the following number: 01202 855856.

Application Forms

Fund Literature

Fund Charges

Semi-Annual Report for the period ended 31 January 2025

Annual Report for the period ended 31 July 2024

Semi-Annual Report for the period ended 31 January 2024

Annual Report for the period ended 31 July 2023

Semi-Annual Report for the period ended 31 January 2023

Annual Report for the period ended 31 July 2022

Semi-Annual Report for the period ended 31 January 2022

Annual Report for the period ended 31 July 2021

Semi-Annual Report for the period ended 31 January 2021

Annual Report for the period ended 31 July 2020

Semi-Annual Report for the period ended 31 January 2020

Annual Report for the period ended 31 July 2019